Instant Cash Back On Same‑Day Cash Advance Apps: The ‘Right Now’ Rescue Move Reviewers Say Beats Overdraft Fees

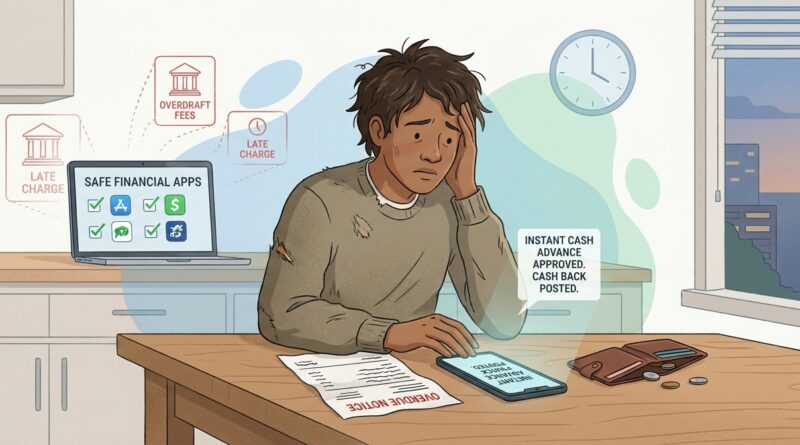

You know the feeling. A bill is due today, your account is a little short, and the bank transfer you started is moving at the speed of cold syrup. That is when people start searching for an instant cash advance app same day cash back option and end up in a mess of half-answers, hidden express fees, and offers that look a lot like payday loans with better branding. The good news is that a few cash advance apps really can send money the same day, sometimes within minutes, if your bank and debit card qualify. The less-good news is that many of them make “instant” a paid extra, and some nudge you toward monthly memberships you may not need. If your goal is simple, cover a bill today without getting hit with an overdraft fee tomorrow, you need to know which apps move fast, what they actually cost, and where cash back can soften the hit a little.

⚡ In a Hurry? Key Takeaways

- Yes, some cash advance apps really do offer same-day or near-instant transfers, but “instant” often costs extra.

- Check three things first: your bank connection, the app’s express transfer fee, and whether you are being pushed into a subscription.

- The safest move is to use a small advance only for a true short-term gap, then pair it with debit-card cash back or a promo to reduce the sting.

Why people are turning to these apps right now

Most people are not using cash advance apps because it sounds fun. They are using them because the alternative is worse.

An overdraft fee can be $30 or more. A late utility payment can pile on extra charges. A missed minimum payment can hurt your credit. Against that, a small fast advance can look like the least bad option.

That is the real comparison here. Not “Is borrowing ideal?” It usually is not. The question is whether a same-day advance is cheaper and less damaging than the fee train coming at you.

What “same day” really means

This is where a lot of review roundups get fuzzy.

Standard transfer

Usually free, but often takes 1 to 3 business days. That does not help much if the bill is due at 5 p.m.

Express or instant transfer

This is the fast option. Some apps can send funds to a linked debit card in minutes. Others say “same day” but mean later that evening, or only on business days.

Bank eligibility matters

Even if the app supports instant delivery, your bank or debit card has to support it too. If not, you may get bumped back to the slower route.

So if you need money today, do not stop at the app store description. Check the transfer method inside the app before you count on it.

The big trade-off: speed versus fees

Here is the plain-English version.

Many cash advance apps advertise low-cost access to your paycheck early or a small advance with no traditional interest. That sounds good. But when you need the money right away, the express fee is where the real cost shows up.

Common charges can include:

- Instant transfer fees

- Monthly membership fees

- Optional tips that do not always feel optional

- Out-of-network ATM fees if the app uses its own card

If an app charges $4.99 to $9.99 for instant delivery, that still may be better than a $35 overdraft. But you should do the math before tapping “confirm.”

Which kinds of apps are usually fastest

Brand details and terms change often, but most same-day options fall into a few buckets.

1. Cash advance apps tied to your paycheck history

These look at your linked bank account, deposits, and spending patterns. If approved, they may offer small advances and instant delivery for a fee.

Best for: covering a short gap before your next paycheck.

Watch for: low starting limits, subscriptions, and tipping prompts.

2. Employer-linked earned wage apps

If your job supports one of these services, they can be one of the cleaner options because you are often accessing wages you have already earned.

Best for: predictable payroll workers.

Watch for: employer participation requirements and limited transfer windows.

3. Fintech apps with debit card features and rewards

Some newer apps blend small advances, early direct deposit, spending accounts, and cash back. These can be useful if you need today’s bill covered and want to earn a little back on future debit card spending.

Best for: people willing to use one app for several money tasks.

Watch for: account-switching hassle and reward rules.

Where the “cash back” part actually fits in

Let’s be honest. Cash back is not going to magically erase a cash crunch. But it can help if you use it the right way.

Some apps offer cash back on debit card purchases, bill pay categories, gas, groceries, or partner merchants. If you are already using the app’s card or linked spending feature, that can put a few dollars back in your pocket over time.

That matters when you are trying to stay out of the fee spiral.

If you are also looking at fast signup offers, it is worth reading Instant Cash Back On Limited‑Time Card Promos: The ‘Right Now’ Signup Trick Reviewers Say Beats Waiting For Points. It is a different tool than a cash advance, but in some situations a quick promo plus normal spending can be a smarter move than borrowing again next week.

How to pick the least painful option

When you are stressed, everything starts to look urgent. Slow it down for two minutes and check these five things.

Transfer timing

Does the app say “instant,” “within hours,” or “1 business day”? Those are not the same thing.

Total cost today

Add the instant fee, membership fee, and any tip. Compare that total to the overdraft or late fee you are trying to avoid.

Advance amount

Many first-time users get a lower limit than they expected. If you need $200 and the app offers $40, it may not solve the actual problem.

Repayment date

Most apps pull repayment automatically on your next payday. Make sure that will not leave you short all over again.

Bank compatibility

If your bank connection is flaky, your “instant” rescue plan may turn into a waiting game.

A simple strategy if you need money today

Here is the practical play.

- Figure out the exact amount needed to avoid the fee or shutoff. Not an estimate. The real number.

- Use the smallest same-day advance that solves that one problem.

- Choose the app with the lowest all-in cost for instant delivery, not just the best ad copy.

- If the app offers debit-card rewards or cash back on spending you already do, use that to chip away at future shortfalls.

- Turn off any optional extras you do not need, especially subscriptions you forgot you signed up for.

The key is not to turn a one-time bridge into a monthly habit.

Red flags to avoid

There are a few signs an offer is drifting from “helpful short-term tool” into “expensive mistake.”

- The app will not clearly show the fee before transfer.

- You need a paid plan just to access basic features.

- The advance amount is tiny, but the express fee is still chunky.

- The app keeps nudging you to tip higher.

- The product starts to look like a payday loan with aggressive repayment terms.

If you feel rushed, that is usually the exact moment to get more careful.

At a Glance: Comparison

| Feature/Aspect | Details | Verdict |

|---|---|---|

| Same-day funding | Often available through instant debit-card transfer, but many apps charge extra and bank compatibility matters. | Useful if the fee is lower than your overdraft or late charge. |

| Cash back value | Usually comes through debit-card spending rewards, merchant offers, or promo bonuses, not the advance itself. | Nice bonus, but not a reason by itself to borrow. |

| Hidden costs | Watch for subscriptions, express fees, optional tips, and auto-repayment timing. | This is where good apps and bad deals separate fast. |

Conclusion

If you are searching in a panic for instant cash, you are exactly the person most likely to get buried in fine print. That is why it helps to keep the goal small and clear. Find the app that can actually pay out same day, check the real fee for speed, skip any paid extras you do not need, and use cash back as a bonus rather than the main reason to borrow. Done carefully, a short-term advance can be the cheaper move compared with overdraft fees, late charges, or service shutoffs. The point is not to make borrowing feel fun. It is to get through a tight spot today without falling into a much bigger hole tomorrow.